Starting a new restaurant business is a dream for most people, but it can be tough if you do not know what you are doing.

Starting a new restaurant business is a dream for most people, but it can be tough if you do not know what you are doing.

Loan expert ARF Financial notes that overlooking key steps like designing a business plan, getting proper financing through a loan now, pay later scheme, or choosing the right people now, could mean that you would have to pay a lot more later to keep your new restaurant afloat.

Here are a couple of tips to make sure you take that first step to the road to restaurant success right.

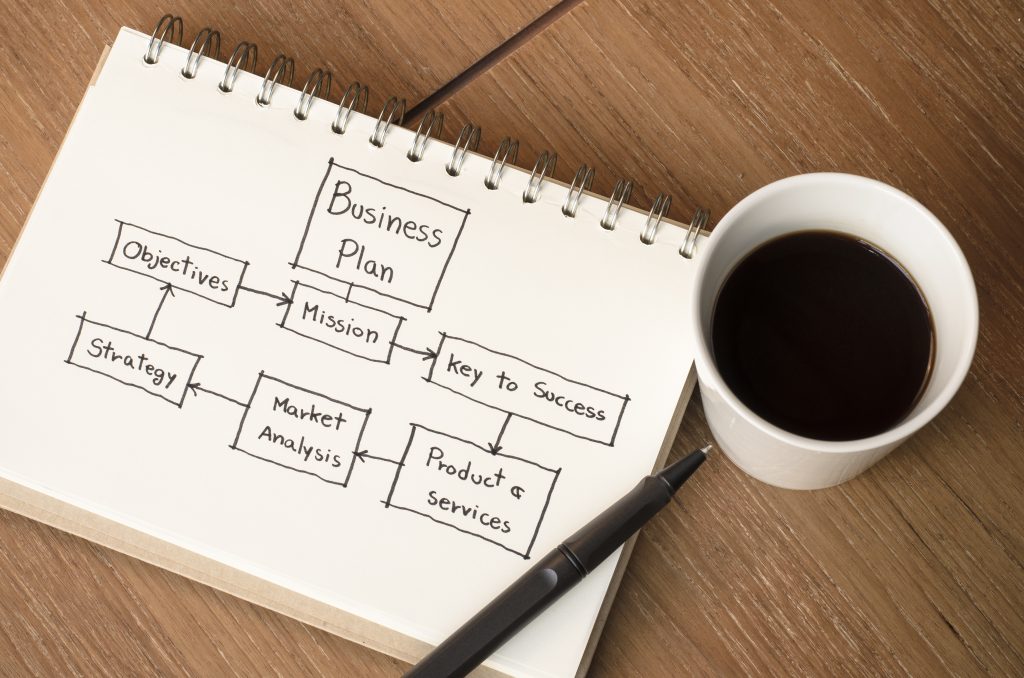

Design the Right Business Plan

A business plan is more than just coming up with a concept and a restaurant name. A carefully designed business plan has those two items, but should also have details like your restaurant’s location, menu, as well as finances.

Some market research and information would also be helpful in making your plan an essential road-map to success for you, your employees, and even your investors.

Set Your Finances Straight

Considering that starting a new restaurant can be a huge financial risk, making sure you have secured enough capital to enact your business plan is one of the first things you should do as soon as you have done it.

As much as the temptation is there to fund everything on your own dime, getting a loan from a bank or investors to help fund your dream eases the financial burden on you personally.

Get the Right People

We have all experienced bad service from a restaurant, and a bad review due to that can break a startup restaurant. Salaries are also a huge part of your restaurant’s expenses, so you would want to make sure you are paying the right people.

Getting the right staff could mean giving your customers a better dining experience. Taking the time to not only interview but also explaining your business plan and their role in it will make sure you and your staff are on the same page.

Your new restaurant is as much an emotional investment as it is a financial investment. Seeing it succeed is going to be as rewarding as much as it is going to be a lot of work.